How to Increase Your Equity Over the Next 5 Years

Many of the questions currently surrounding the real estate industry focus on home prices and where they are heading. The most recent Home Price Expectation Survey (HPES) helps target these projected answers.

Here are the results from the Q2 2019 Survey:

- Home values will appreciate by 4.1% in 2019

- The average annual appreciation will be 3.2% over the next 5 years

- The cumulative appreciation will be 16.8% by 2023

- Even experts representing the most “bearish” quartile of the survey project a cumulative appreciation of over 6.7% by 2023

What does this mean for you?

A substantial portion of family wealth comes from home equity. As the value of a family’s home (an asset) increases, so does their equity.

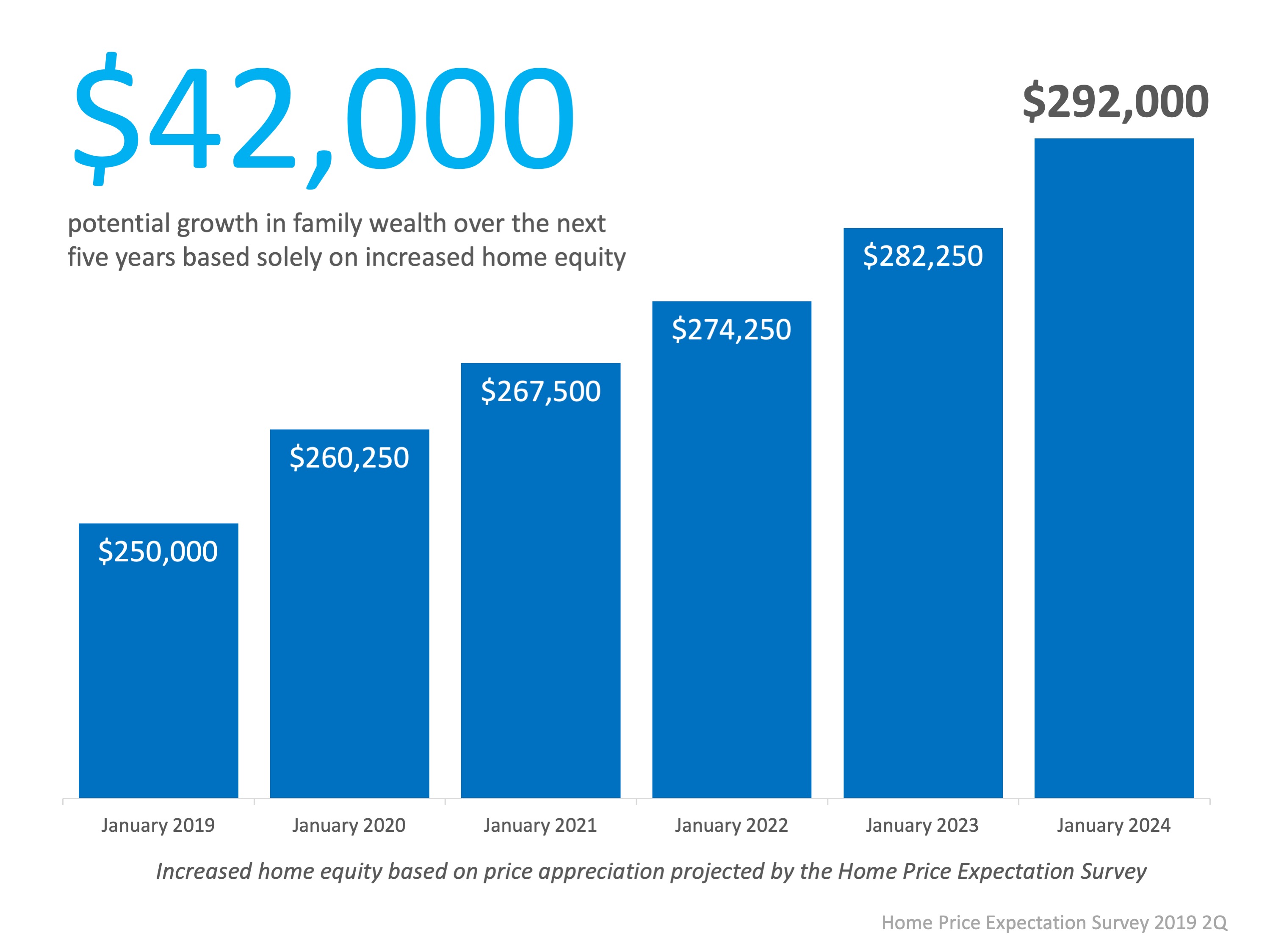

Using the projections from the HPES, here is a look at the potential equity a family could earn over the next five years if they purchased a $250,000 home in January of 2019: Based on gains in home equity, their family wealth could increase by $42,000 over that five-year period.

Based on gains in home equity, their family wealth could increase by $42,000 over that five-year period.

Based on gains in home equity, their family wealth could increase by $42,000 over that five-year period.

Based on gains in home equity, their family wealth could increase by $42,000 over that five-year period.Bottom Line

If you don’t yet own a home, now may be the time to purchase. Owning or moving up to your dream home could allow you to ride the increase in equity of a growing asset.

![Home Prices Up 5.05% Across the Country [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/07/25072858/20190729-MEM-1046x1600.jpg)

![The Cost of Waiting: Interest Rates Edition [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/07/19100001/20190719-MEM-1046x784.jpg)

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/06/24131009/FTHB-Demographics-ENG-MEM-1046x1477.jpg)